Executive summary – what changed and why it matters

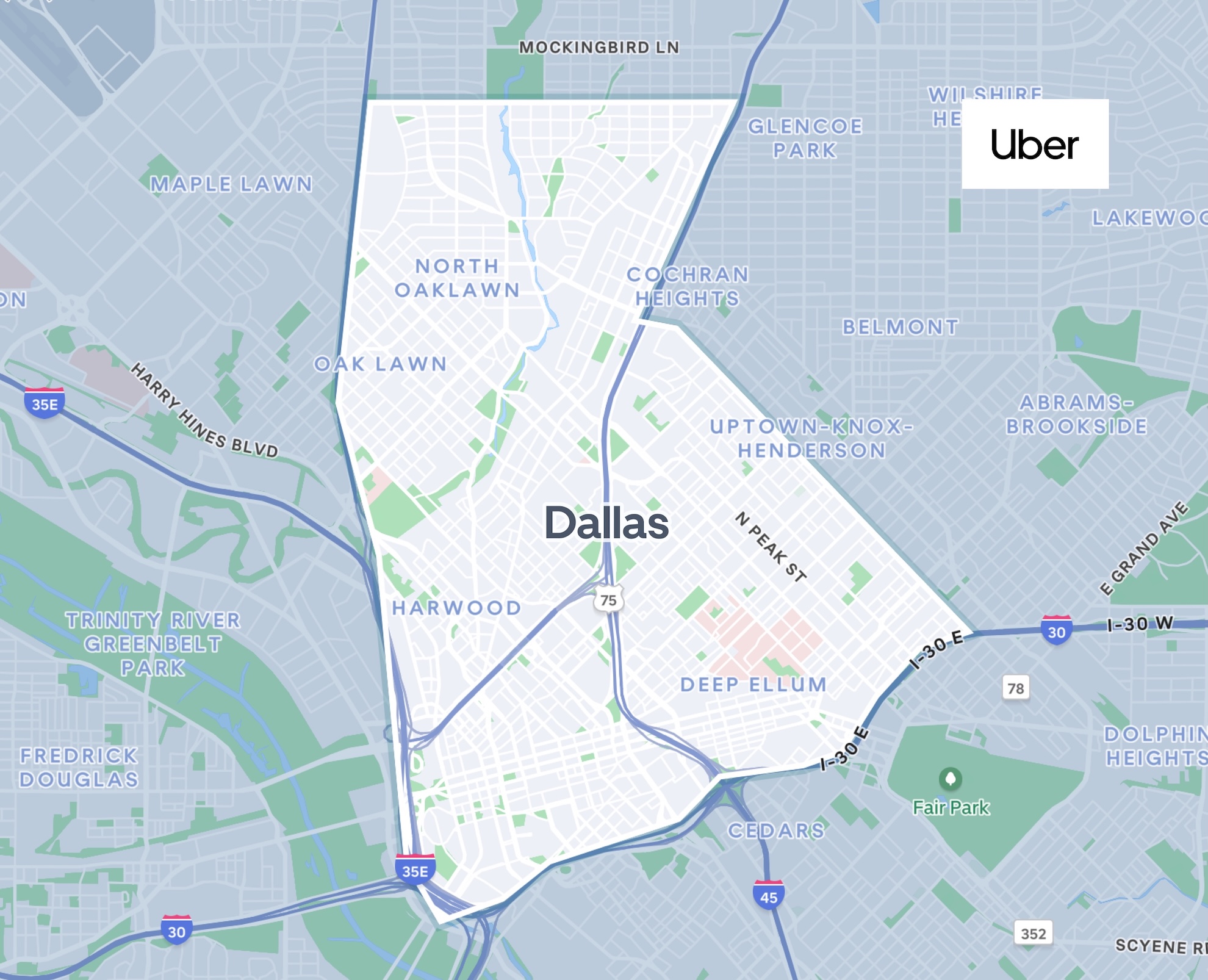

Uber and Avride have launched a commercial Avride‑branded robotaxi service in Dallas using Hyundai Ioniq 5 EVs equipped with Avride’s self‑driving system. Initial operations are limited to a 9‑square‑mile area and include a human safety operator; the partners plan to remove the safety operator and expand geography over time. This move converts a partnership and a $375M strategic capital commitment into a real passenger service and materially advances Uber’s multi‑partner AV strategy.

- Immediate impact: Real-world rider exposure to Avride’s autonomous stack via Uber’s marketplace and support systems.

- Scale signal: Uber intends hundreds of Avride robotaxis in Dallas in the coming years and AVs in at least 10 cities by end‑2026.

- Operational testing: Uber will assume day‑to‑day fleet ops (charging, maintenance, depots) while Avride focuses on vehicle testing and autonomy.

Key takeaways for executives and product leaders

- Substantive change: a commercial robotaxi service is live in an urban downtown geofence – but not yet driverless. That matters because it tests marketplace integration, rider acceptance, and fleet ops before removing human safety oversight.

- Quantified scope: 9 square miles initially; Hyundai Ioniq 5 EVs; plan to scale to “hundreds” in Dallas over a few years; Uber’s AV goal is presence in ≥10 cities by 2026.

- Cost/UX: Robotaxi fares match human‑driver equivalents and riders can opt out at match time; unlocking, trunk and trip start are handled through the Uber app.

- Governance/finance: Avride secured ~$375M in strategic investments/commitments from Uber and Nebius; the deployment tests commercialization of that capital.

- Competitive placement: This brings Avride into the small group (Waymo, WeRide, Nuro) that is commercially operating AV fleets via major partners.

Breaking down the deployment – capabilities and constraints

What’s real today: passenger rides on Avride‑equipped Hyundai Ioniq 5 EVs inside a 9‑square‑mile Dallas area that includes downtown. A human safety operator sits behind the wheel for now. Uber does the rider experience, support and — eventually — routine fleet operations; Avride runs vehicle testing and autonomy development.

What’s promised: removal of the safety operator (full driverless), geographic expansion, and growth to “hundreds” of vehicles in the market over years. Uber’s parallel deals (Waymo, WeRide, Nuro and others) mean it’s assembling a diversified supplier base rather than betting on a single stack.

Why this move matters now

Timing: Uber has spent the last year converting partnerships and investments into pilots; this launch signals a shift from lab pilots to revenue‑facing services. Economically, Uber needs lower per‑trip labor cost and predictable unit economics from AVs; commercially, Avride needs real passenger data and operational scale to improve perception, training datasets and monetization.

Competitive context — how this compares

Waymo and WeRide operate with large, multi‑year deployments and regulatory track records in several cities. Uber’s multi‑partner strategy reduces supplier concentration risk and accelerates city coverage, but it increases integration complexity: multiple stacks, different operational SOPs, and varied safety metrics. Avride’s advantage is a combined sidewalk delivery and robotaxi product pipeline — a potential cross‑sell to Uber Eats and mobility services.

Risks, governance and compliance to watch

- Safety and public perception: Incidents or widely publicized interventions could set back adoption across all of Uber’s AV partners.

- Regulatory/legal: Local approvals, insurance, incident reporting and liability frameworks will determine rollout speed and cost.

- Operational scale: Charging infrastructure, depot throughput, cleaning, and repair cycles must be proven at hundreds‑vehicle scale.

- Data and cybersecurity: Rider data, telemetry and OTA updates add privacy and attack‑surface risk — require audits and SOC/ISO controls.

Operator’s checklist — concrete next steps

- Set clear KPIs for pilots: interventions/disengagements per 1,000 miles, incidents per million vehicle miles, rider NPS and cost per trip (including charging/maintenance).

- Require third‑party safety audits and publish a transparent incident log for the pilot period to build public trust and regulator confidence.

- Validate operational handoffs: measure depot throughput, charge availability, and mean time to repair before scaling to hundreds of vehicles.

- Legal/compliance: map insurance coverage, local operating permits, and data retention rules before expanding geographies.

- Product integration: define marketplace rules (how often robotaxis are matched, opt‑out flows, driver substitution) and track cancellation/acceptance rates.

Bottom line

Uber and Avride’s Dallas robotaxi is an important commercial milestone: it proves marketplace integration and begins operational scaling under real conditions. But it’s still an early‑stage deployment — human safety oversight, a small geofence and limited fleet constraint the immediate business impact. Executives should treat this as a structured pilot: measure safety and ops metrics rigorously, prepare compliance and fleet systems for scale, and avoid conflating “commercial availability” with driverless, at‑scale economics until the data supports it.