Why This Announcement Matters

Kaaj, a 2024 startup founded by risk veterans Shivi Sharma and Utsav Shah, raised a $3.8M seed round and claims its agentic AI can cut small‑business underwriting from days to minutes. Kaaj says it has processed over $5B in applications and that teams handling 500 monthly files could handle 20,000 with the same headcount-a 40x throughput claim. If true at reasonable accuracy and auditability, this changes the unit economics of small loans and reopens previously unprofitable segments for banks, equipment financiers, and fintech lenders.

Key Takeaways

- Material efficiency promise: days to minutes, with a headline 40x throughput potential; early customers include Amur Equipment Finance and Fundr.

- Scope: automates end-to-end credit analysis-document ingestion, classification, tamper checks, policy evaluation-and writes into a lender’s LOS.

- Integrations: works with CRM systems like Salesforce, HubSpot, and Microsoft; designed to fit existing underwriting workflows.

- Market context: competes with point solutions like Middesk (KYB) and Ocrolus (doc processing); Kaaj’s pitch is full-package underwriting automation.

- Governance is the gating factor: lenders must validate explainability, fairness (ECOA/Reg B), and model risk management before scaling.

Breaking Down the Announcement

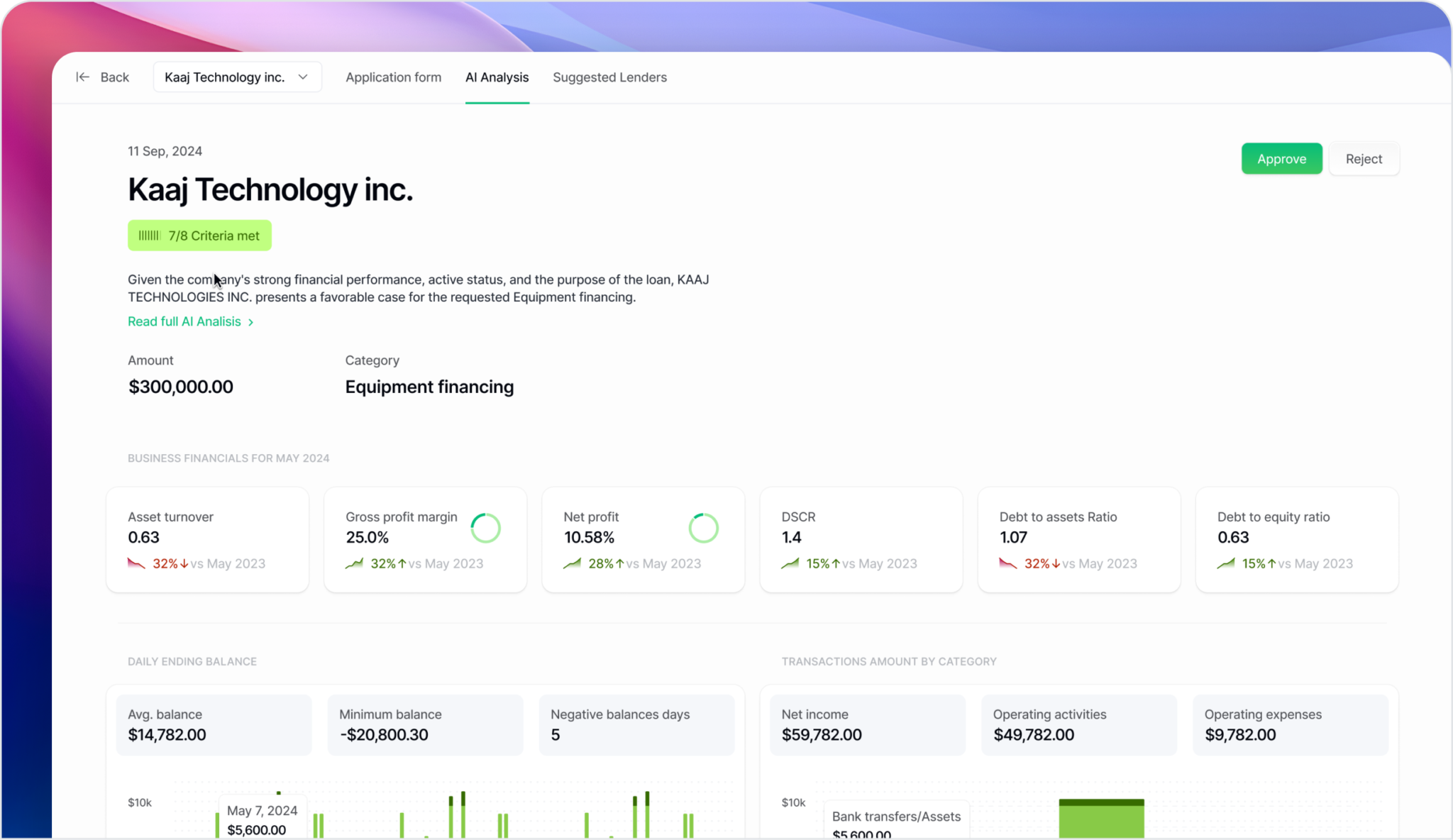

Kaaj’s platform targets the costliest friction in small‑business credit: manual document work and policy checks. Borrowers submit bank statements, tax returns, and financials; Kaaj’s agents identify and classify files, extract and validate fields, screen for anomalies or tampering, and populate the lender’s Loan Origination System (LOS). The system also evaluates packages against lender policies, providing a pass/fail or escalation signal and a structured summary for human underwriters.

The company asserts it has already processed over $5B in applications (note: applications, not funded loans). The promise is to let underwriting teams shift effort from document handling and rote checks to exceptions and deal structuring—especially for lower‑ticket loans where manual review is often uneconomic. By compressing cycle times, lenders can raise straight‑through processing rates and improve pull‑through by issuing faster decisions.

Industry Context and Competitive Landscape

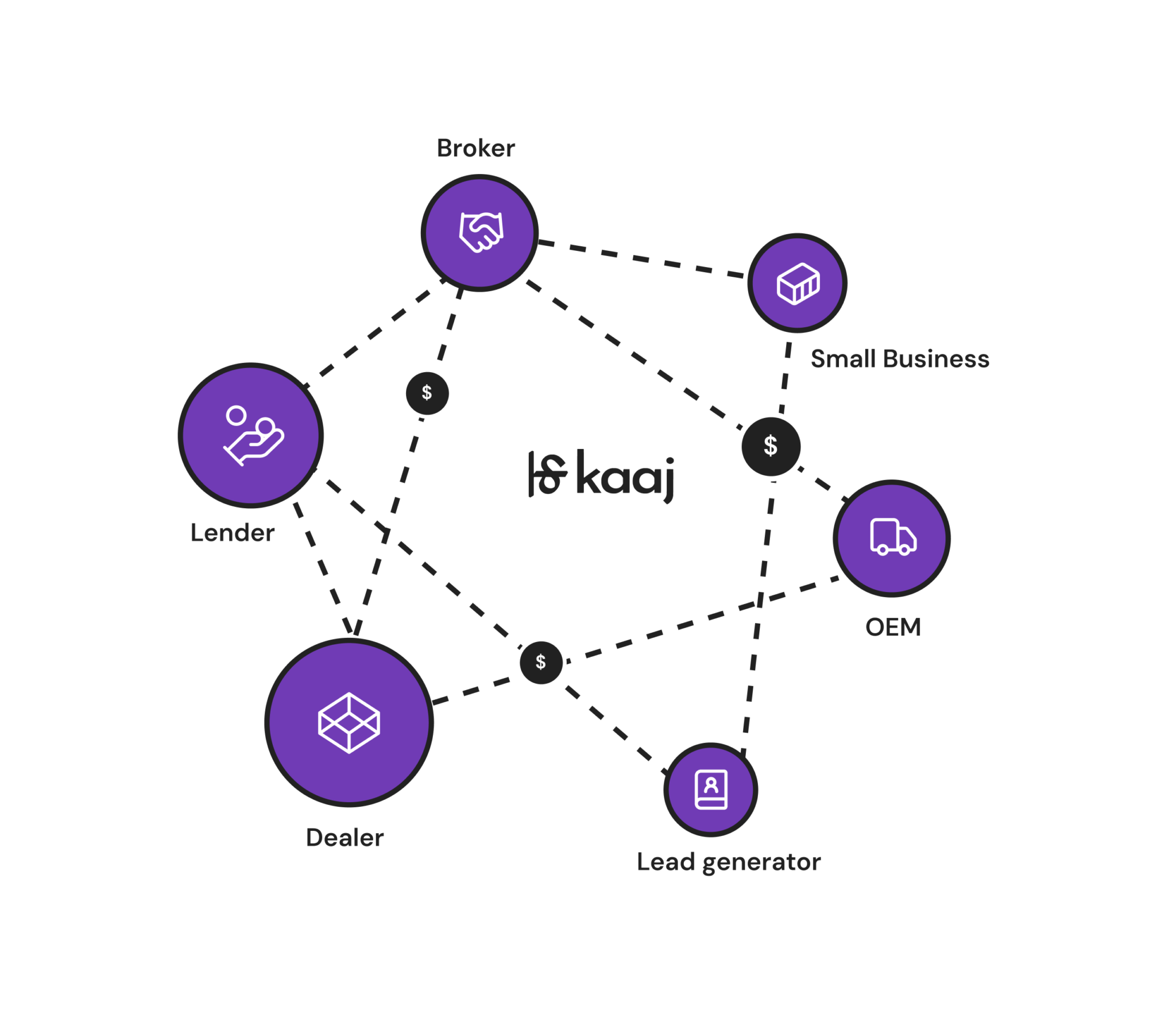

Small‑business lending struggles with adverse unit economics for smaller tickets because manual reviews consume hours per file. Vendors like Ocrolus reduce that burden with document classification and human‑in‑the‑loop extraction; Middesk focuses on KYB and business identity; MoneyThumb parses financial statements. Kaaj’s differentiation claim is “end‑to‑end” automation that not only parses documents but also evaluates policy and flags fraud, wrapped in agentic workflows that mimic an underwriting team’s steps.

Why now: lenders are pushing for cost‑out in back offices amid rising fraud and tighter credit, while agentic LLM patterns are maturing enough to orchestrate multi‑step tasks with tool use and guardrails. The open question is whether “end‑to‑end” really reaches committee‑grade decisions or mainly triages and assembles reasoned packets for human sign‑off. In comparable deployments, straight‑through processing often starts modest and increases as policies, data sources, and exception handling are tuned.

Risk, Compliance, and What to Validate

Credit is a regulated decision domain. Any AI system operating here must satisfy:

- Explainability and adverse action: ECOA/Reg B requires specific reason codes for denials or counteroffers. Lenders need deterministic policy mappings and stable, auditable reason generation.

- Model Risk Management: Banks following SR 11‑7/OCC 2011‑12 will require model inventories, validation packages, performance monitoring, and change controls for agent workflows and extraction models.

- Fair lending: Document and policy automation can create disparate impact if data quality varies across applicant segments. Run pre‑deployment bias testing with appropriate proxies and monitor outcomes over time.

- Fraud controls: Tamper detection is critical amid synthetic bank statements. Validate Kaaj’s methods (e.g., PDF structure checks, cross‑document consistency) and, where possible, corroborate with first‑party bank data feeds.

- Data security and vendor risk: GLBA scope applies. Expect SOC 2 Type II, encryption at rest/in transit, PII minimization, and robust audit logs of every agent action and tool call.

Operationally, watch failure modes typical to agentic systems: prompt injection via embedded document content, tool‑use loops that increase latency, and occasional hallucinated fields if extraction confidence thresholds are too low. In production, you’ll want calibrated confidence scores, human‑in‑the‑loop for exceptions, and a clear escape hatch back to manual processes.

What This Changes for Operators

If Kaaj’s performance holds up under audit, lenders can profitably revisit smaller tickets in equipment finance, working capital, and broker‑driven packages that arrive as unstructured PDFs. Faster cycle times also improve broker relationships and win rates in competitive auctions, where decision speed is a differentiator. However, “end‑to‑end” rarely means zero‑touch for all files; expect automation to cover routine, well‑documented cases first, with humans handling thin‑file, inconsistent, or policy‑edge scenarios.

Compared to adopting multiple point solutions (doc extraction + KYB + decisioning), a consolidated workflow can simplify vendor management and reduce integration cost. The trade‑off is concentration risk and the need to verify that each module—extraction, fraud screening, policy evaluation—meets your internal standards individually, not just in aggregate.

Recommendations

- Start with a controlled pilot on a single product (e.g., small‑ticket equipment finance). Track straight‑through processing rate, decision latency, extraction accuracy, and adverse action reason quality.

- Demand a full model risk package: documentation of agent workflows, training data provenance for extraction models, validation results, monitoring plans, and change‑management procedures.

- Harden governance: implement role‑based access, immutable audit logs of every field transformation, and confidence‑based human review thresholds. Red‑team for prompt injection via uploaded documents.

- Plan integrations early: align Kaaj with your LOS and CRM, and consider adding bank‑data connections for corroboration. Set SLAs for exception handling to prevent backlog when volumes spike.

Bottom line: Kaaj’s raise and rapid traction signal a credible push to automate the entire SMB credit packet, not just parse documents. The upside—lower unit costs and faster decisions on smaller loans—is real. The limiter will be governance: lenders that can operationalize explainable, auditable agentic workflows will move first; others should pilot now and scale once the controls prove out.